Fixed Deposits (FDs) have long been a cornerstone of safe investments in India. Popular for their guaranteed returns, simplicity, and capital safety, FDs appeal to risk-averse investors seeking predictable growth.

However, as the financial landscape evolves, understanding how to maximize your returns through favorable fixed deposit interest rates is key.

This blog will tell you how interest rates in FD investments work, strategies to get the most out of your FDs and compare them to other investment options like Mutual Funds to make informed financial decisions.

Understanding Fixed Deposit Interest Rates

Fixed deposit interest rates are the backbone of FD returns. These rates are typically fixed at the time of deposit, ensuring your earnings remain unaffected by market fluctuations. Banks and financial institutions periodically revise these rates based on factors like:

- Repo Rates: Interest rates in FD schemes often align with the Reserve Bank of India’s (RBI) repo rate adjustments. When repo rates increase, FD interest rates tend to follow suit.

- Economic Factors: Inflation, liquidity, and government policies also influence fixed deposit interest rates.

- Tenure of Investment: FDs with longer tenures generally offer higher interest rates than short-term deposits.

- Type of Financial Institution: Public sector banks, private banks, and non-banking financial companies (NBFCs) offer varying rates, with NBFCs often providing slightly higher interest rates for FDs.

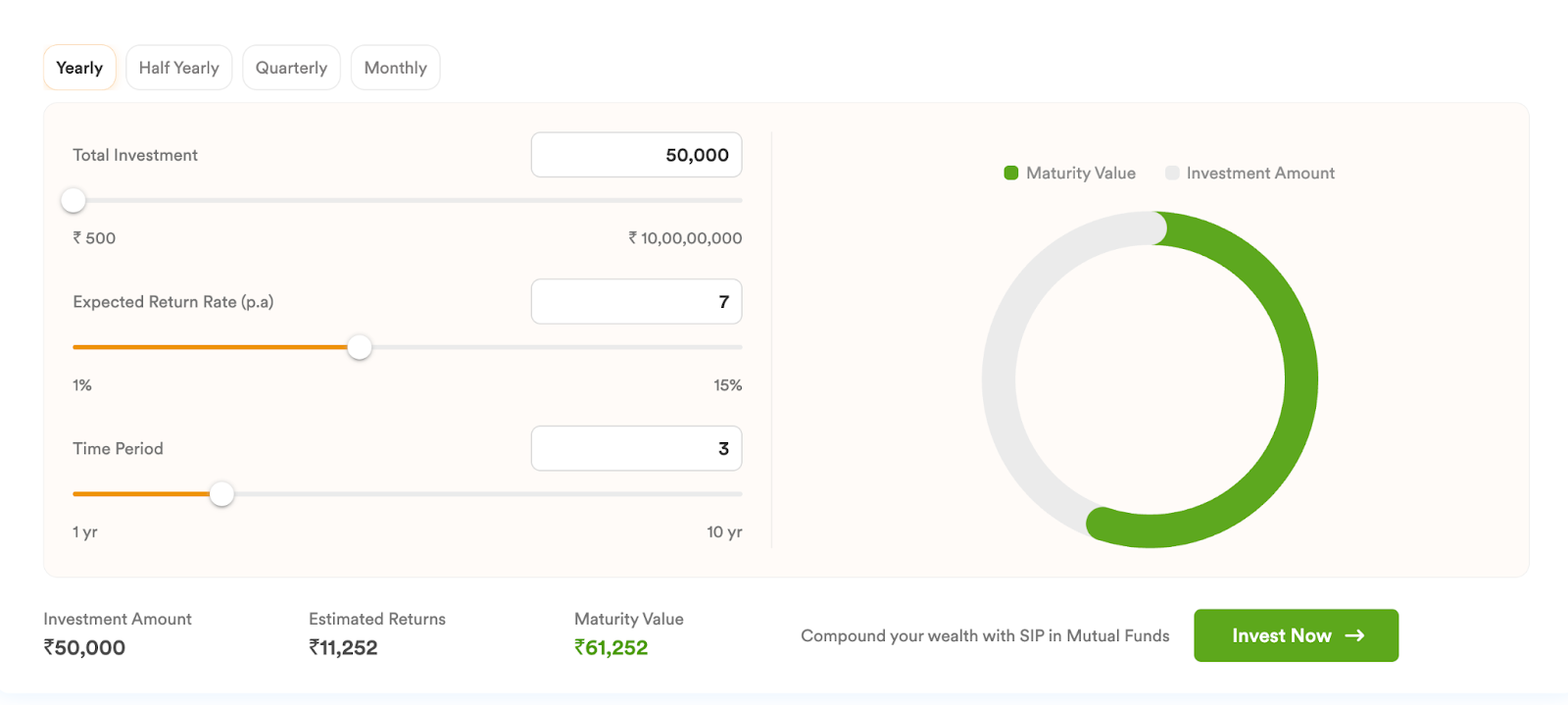

Calculate your FD interest rate on Dhan’s FD Calculator.

Tax Implications of Fixed Deposits

FD interest earnings are subject to taxation and are categorized as “Income from other sources.” If your interest income exceeds ₹40,000 in a financial year (₹50,000 for senior citizens), Tax Deducted at Source (TDS) will apply.

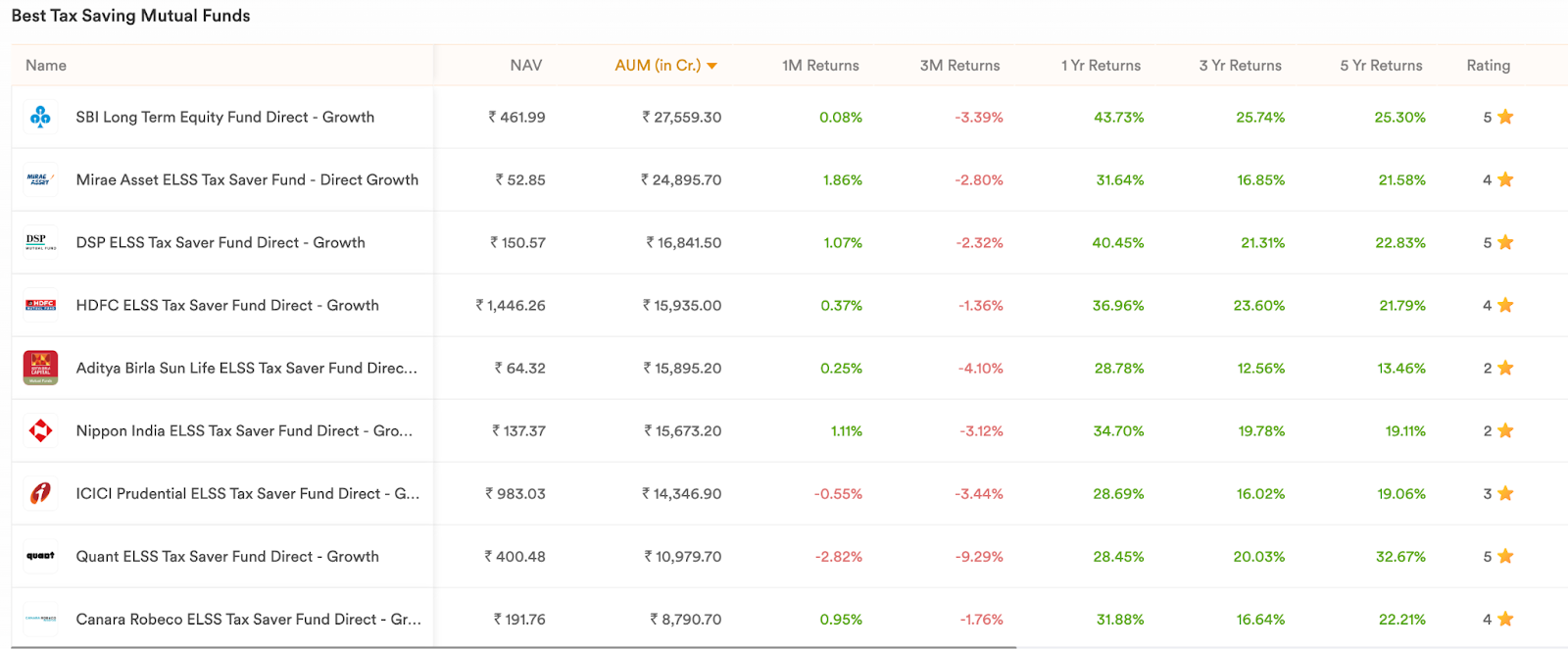

Equity Linked Savings Schemes (ELSS) are a popular category of Mutual Funds that not only offer the potential for higher returns but also help you save on taxes. Investments in ELSS qualify for deductions of up to ₹1.5 lakh under Section 80C of the Income Tax Act.

Invest in Tax-Saving Mutual Funds & Maximize Your Returns

These funds come with a relatively short lock-in period of three years, the lowest among other tax-saving instruments, and offer the added benefit of equity market growth.

The Role of Inflation in Fixed Deposit Returns

While FDs offer safety, inflation can erode the purchasing power of your returns. For instance, if your FD earns a 7% interest rate and inflation is 6%, your real return is only 1%.

To combat inflationary pressures, consider complementing FDs with other investment options like Mutual Funds or equity investments, which have the potential to generate inflation-beating returns over time.

But, Are Fixed Deposits better than Mutual Funds Returns?

Fixed Deposits offer stable but limited returns, ranging between 6-8% annually. Mutual Funds, depending on the type, can yield significantly higher returns over the long term:

- Equity Mutual Funds: Historically, these have delivered 12-15% annualized returns over 5-10 years.

- Debt Mutual Funds: Though safer than equities, these can offer 7-10% returns while still outperforming most FDs.

Let’s look at a few factors and compare both mutual funds and fixed deposits.

Risk

- FDs are risk-free, making them ideal for conservative investors.

- Mutual Funds involve market risks, but the potential for higher returns often outweighs this for long-term goals.

Liquidity

- FDs can be broken prematurely but often incur penalties.

- Mutual Funds are more liquid, allowing redemptions without penalties (except for certain close-ended schemes).

Tax Efficiency

While FD returns are fully taxable, certain categories of Mutual Funds (like Equity Linked Savings Schemes or ELSS) offer tax benefits under Section 80C and more favorable taxation on long-term gains.

What’s the verdict then?

To keep things simple, here is a visual representation of how a sum investment of 10,000 would look like in FD vs Mutual Funds over a course of 10 years:

*Avg Market Returns have been considered for the calculation of returns

While FDs are the go-to for safety, Mutual Funds outperform FDs in terms of returns, tax efficiency, and inflation-adjusted growth, making them a suitable alternative for medium to long-term investments.

Also Read: History of Mutual Funds in India

Balancing Fixed Deposits with Market-Based Investments

While FDs are synonymous with safety, relying solely on them may hinder your wealth creation goals. A diversified approach can help achieve a balance between risk and returns.

- Mutual Funds for Growth: With tailored options like equity, debt, or hybrid funds, you can match your risk appetite and time horizon for optimal returns.

- Stock Market for Potential Wealth: Direct equity investments, though riskier, offer the highest returns over the long term for those willing to weather market fluctuations.

Also Read: How to Start Trading in the Stock Market?

By integrating market-based instruments with your fixed deposits, you can secure a stable income while building a portfolio that grows faster than inflation.

Conclusion

Fixed Deposits remain a reliable and straightforward investment for risk-averse individuals. By strategically choosing tenures, comparing interest rates, and leveraging tax-saving options, you can maximize your returns on FDs. However, their limited growth potential and susceptibility to inflationary pressures make them less ideal for long-term wealth creation.

In contrast, Mutual Funds and stock market investments, though subject to market risks, offer significantly higher returns and inflation-adjusted growth. To truly maximize your financial potential, consider balancing the safety of FDs with the growth potential of Mutual Funds.

After all, when it comes to wealth creation, staying safe is wise, but taking calculated risks is rewarding.

Explore over 1200+ Direct Mutual Funds on Dhan, and start investing at 0% Commissions!