Financial freedom means being able to do what you want, where you want when you want.

However, it is not something that can be done in a single day. It requires setting goals in advance, maintaining proper discipline, and making the right financial decisions.

Financial planning emphasizes that financial freedom does not only involve earning more money but also knowing when to invest and how to preserve it. I

n this blog, we will explore the key steps an individual needs to take now to achieve financial freedom.

1. Set Clear Financial Goals

The first step in financial planning tips is determining the specific type of financial aspiration one has for oneself in the future. To some, it might imply having the freedom to retire early and go on a world tour.

For others, it might provide the luxury of not carrying debt or the flexibility of pursuing their job of interest or desired lifestyle without having to bother about the financial aspect.

When a person writes their objectives down, it helps in making financial goals achievable and breaking them down into measures that they can follow to achieve them.

2. Create and Stick to a Budget

A budget is the foundation of any solid financial management strategy. Therefore, when one fails to track the money that is being earned or spent, one will find him or herself facing so many challenges such as incurring a lot of debts which make them lose their financial freedom.

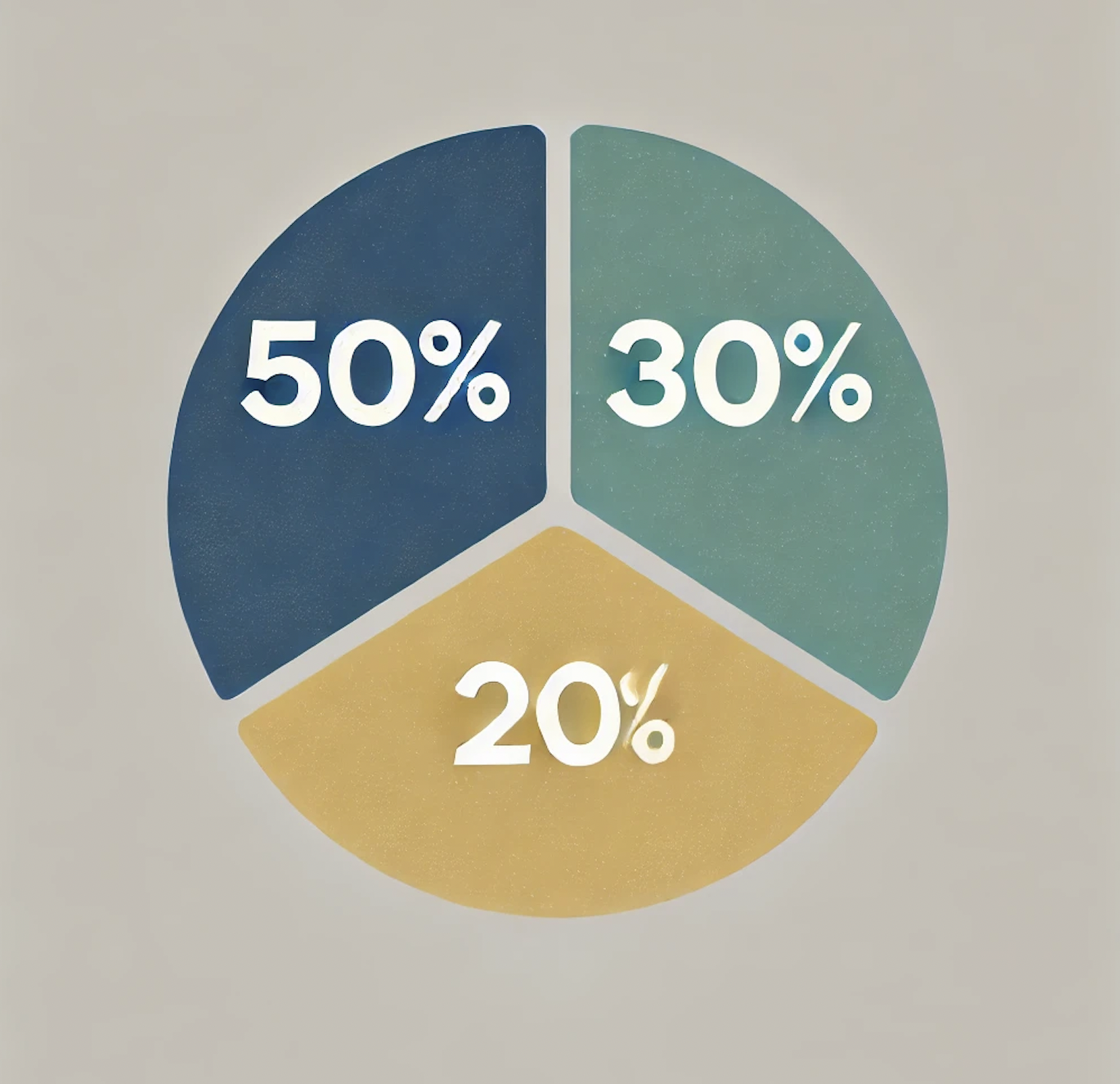

When individuals establish a budget, they feel relaxed and can make decisions regarding the use of money wisely. Consequently, applying the 50-30-20 rule would help divide costs across three different categories.

- 50% for needs

- 30% for wants

- 20% for savings and investments

3. Build an Emergency Fund

An emergency fund acts as a financial cushion, providing a safety net in case of unexpected events like job loss, medical emergencies, or urgent repairs.

Having a sufficient emergency fund means that the person won’t have to rely on credit cards or loans in difficult times, keeping them on track toward financial freedom. Generally, emergency funds include at least 3 to 6 months’ worth of living expenses.

4. Pay Off Debt and Avoid New Debt

Debt is a major hindrance to financial freedom. High-interest debts, such as credit card balances or personal loans, can erode wealth and prevent a person from saving and investing in the future. The sooner they eliminate debt, the faster they’ll be on their way to financial independence.

Once all their high-interest debt is cleared, they should focus on paying down other loans like student loans or mortgages.

Read in detail: How to Reduce Debt

5. Start Investing Early

Investing is one of the most powerful tools in achieving financial freedom. Simply saving money is not enough, as inflation erodes its value over time. Investments, however, grow the wealth by providing returns that beat inflation, helping them accumulate assets over time.

The key to successful investing is starting early, staying consistent, and letting compounding work for an investor.

6. Make Use of Tax-Advantaged Accounts

Tax-saving investments not only help a person reduce their taxable income but also help them in growing wealth for the future.

India offers several tax-saving options to its citizens under Section 80C of the Income Tax Act and other parts of the Income Tax Act. Some Popular Tax-Saving Instruments are:

- ELSS (Equity Linked Savings Scheme)

- Public Provident Fund (PPF)

- National Pension System (NPS)

These options not only reduce the tax liability but also help a person save for their retirement and long-term goals.

Also Read: Fixed Deposits vs. Savings Accounts vs. Mutual Funds – Which One Suits Your Goals?

7. Increase Your Income Streams

While saving and investing are important, increasing income is equally vital for achieving financial freedom. Relying on a single source of income can be risky and limits a person’s ability to accumulate wealth. Therefore everyone should consider expanding their income streams.

Whether it’s freelancing, consulting, or starting an online business, a side hustle can provide additional cash flow. The more they earn, the more they can invest, ultimately accelerating their journey toward financial freedom.

8. Plan for Retirement

Even though retirement may seem far off, it’s best to start planning now. As India’s workforce ages, it’s important to ensure that a person has a financial cushion when they can no longer work.

The sooner they start saving for retirement, the less they’ll need to save each month to reach their retirement goals. By investing consistently in retirement plans, they can enjoy a comfortable life after they stop working.

Read: How Much Money Do You Need for Retirement?

9. Protect Your Wealth with Insurance

One of the key aspects of financial freedom is securing the assets and their loved ones against unexpected financial burdens.

Health emergencies, accidents, or the untimely death of a breadwinner can jeopardize financial goals if not properly insured. Adequate insurance coverage ensures that life’s uncertainties don’t derail their journey to financial freedom.

10. Regularly Review Your Financial Plan

Achieving financial freedom requires ongoing effort. Life circumstances change, markets fluctuate, and financial goals evolve. It’s important to review the financial plan regularly to make adjustments according to the current market situation and your financial position.

Reviewing your financial plan helps you in ensuring that your investments are aligned with your financial goals and risk tolerance.

Conclusion

Achieving financial freedom requires a clear vision, disciplined planning, and consistent action. By following the steps outlined above, such as setting goals, budgeting, investing, and protecting your wealth, you can steadily move toward a life of financial independence.

The journey to financial freedom is a long one that requires strong determination and discipline. With the right strategy, they can turn their dreams of financial independence into a reality.