Reducing your taxable income while simultaneously building wealth for the future is a goal for many financially aware people.

While various tax-saving instruments are available, two popular categories often come into comparison: Equity-linked saving schemes (ELSS) and traditional tax-saving options.

However, for better understanding which of the two options will better suit the needs of an investor? In this blog, we will compare ELSS with traditional tax-saving options.

ELSS vs. Traditional Tax Saving Options

Among the various options available under Section 80C of the Income Tax Act, two broad categories often dominate the scene, namely the Equity Linked Savings Schemes (ELSS) and traditional tax-saving instruments.

Both of them are discussed below:

What is the ELSS Tax Saver Fund?

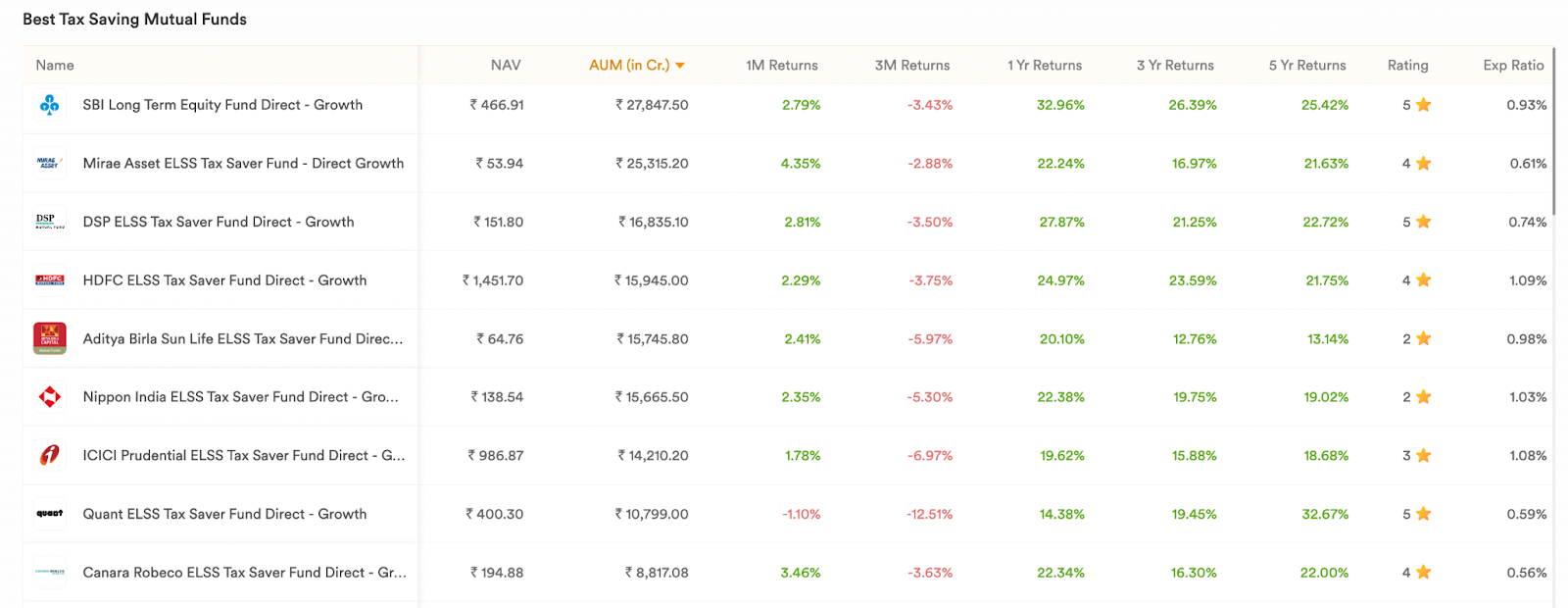

Discover Top ELSS Mutual Funds

ELSS stands for Equity Linked Savings Scheme. They combine the advantages of tax deductions of up to Rs. 1.5 lakh under Section 80C with equity investment benefits. ELSS is an attractive choice for long-term investors due to its tax savings, 3-year lock-in period, and potential for gains.

Read in detail: What are ELSS Funds? A Complete Overview

What are Traditional Tax Saving Options?

These are primarily debt-based instruments offered by the government or banks.

They provide relatively stable returns and are considered low-risk investments. Examples include Public Provident Fund (PPF), National Savings Certificate (NSC), tax-saving fixed deposits (FDs), and Employee Provident Fund (EPF).

Advantages of ELSS Funds

Now that you know what is tax saving mutual funds, here are some advantages offered by them:

Potential for Competitive Returns

ELSS funds have the potential to generate better returns compared to traditional debt instruments, especially over the long term as they invest in the equity market.

Short Lock-in Period

ELSS has the shortest lock-in period of just 3 years, among all tax-saving options under Section 80C. They offer better liquidity as compared to traditional options.

Suitable for Long-Term Goals

ELSS is well-suited for investors with long-term financial goals like retirement planning, children’s education, or wealth accumulation.

Disadvantages of ELSS Funds

ELSS funds have several disadvantages, including:

Market Risk

ELSS investments are equity-linked, therefore investments in ELSS funds are susceptible to changes in the market. In ELSS funds investments capital loss is possible, especially when the market is down.

Not Ideal for Risk-Averse Investors

ELSS funds are excessively volatile, therefore investors with limited risk tolerance may prefer the stability of conventional options over ELSS funds.

Advantages of Traditional Tax-Saving Investment Options

Traditional tax-saving investment options have several benefits:

Safety and Stability

Traditional options like FDs or bonds are less vulnerable to fluctuations in the market. They provide steady, predictable returns and a high degree of safety.

For example, deposits with scheduled commercial banks in India are insured up to ₹5 lakh by the Deposit Insurance and Credit Guarantee Corporation (DICGC). Government-backed schemes like PPF and NSC carry sovereign guarantees, further enhancing their safety.

Suitable for Risk-Averse Investors

For investors who value capital preservation and are uncomfortable with market risks, traditional options can be an ideal choice.

Traditional investments like PPF provide returns at a fixed rate, which are known at the time of investment making them suitable for risk-averse investors.

Disadvantages of Traditional Tax-Saving Investment Options

The following are some disadvantages of traditional tax-saving options:

Lower Returns

Compared to ELSS, traditional options generally offer lower returns. These returns might sometimes struggle to outpace inflation, leading to a decrease in real returns over time.

Longer Lock-in Periods

Longer lock-in periods are a common feature of traditional options, which limits their flexibility and liquidity.

For example: PPF has a lock-in period of 15 years, which is one of the longest among tax-saving instruments. While partial withdrawals are allowed from the 5th financial year onwards. However, this long lock-in period may not be ideal for those seeking flexibility or quick access to their funds.

Which Option Should You Choose?

A person’s financial goals, risk tolerance, and investment terms all play a crucial role in their decision between ELSS and traditional options.

If an investor has a longer investment horizon (5+ years), a higher risk tolerance, a desire for potentially larger returns, and is at ease with market volatility, they can choose ELSS funds.

However, if they are risk averse, value capital preservation, have short- to medium-term financial objectives, and like steady and predictable returns, they can go with traditional options.

An investor can consider the following differences before making any investment decision between the ELSS and the traditional funds. This will also help you understand what tax benefit is applicable in ELSS mutual funds.

| Feature | ELSS | Traditional Options (PPF, NSC, Tax-Saving FDs) |

| Investment Type | Primarily Equity-oriented | Primarily Debt-oriented |

| Returns | Potentially high, market-linked, volatile | Relatively stable, fixed or pre-defined returns, less volatile |

| Risk | High (market risk) | Low (relatively safe) |

| Liquidity | Highest among 80C options (3-year lock-in) | Lower liquidity, varying lock-in periods (5-15 years typically) |

| Tax Benefit | Deduction under Section 80C (up to ₹1.5 lakh) | Deduction under Section 80C (up to ₹1.5 lakh) |

| Taxation of Returns | Long-term capital gains tax (LTCG) at 12.50% on gains above ₹1.25 lakh/year | Interest income is taxed as per the individual’s income tax slab |

| Lock-in Period | 3 years | Varies: PPF (15 years), NSC (5 years), Tax-Saving FDs (5 years) |

| Suitability | Long-term goals (5+ years), higher risk tolerance | Short to medium-term goals, lower risk tolerance, stable returns desired |

Conclusion

There are advantages and disadvantages to both ELSS and traditional tax-saving options. ELSS funds have market risk but they also have the potential for larger returns and a shorter lock-in period. Traditional options offer stability and safety but also have longer lock-in periods and lower returns.

Therefore before choosing, every investor should carefully analyze their financial objectives, investment horizon, and risk tolerance to make a better decision.