Options trading is considered to be one of the most challenging forms of trading because of its complexity. There are many concepts that an options trader must know if they want to trade options online. One of these concepts is Options Greeks.

What are Option Greeks: Option Greeks Explained

Option Greeks are financial measures of the sensitivity of an options price to its underlying asset. Each and every Options Greek is widely used while buying or selling the different types of options in trading.

Jog back to your classroom in school. You must’ve learned some mathematical formulae that were more important than others. Similarly, there are five Greeks in options trading that are used extensively while analyzing options contracts. These include:

1. Delta

2. Gamma

3. Vega

4. Theta

5. Rho

These measures are considered very essential to make informed options trading. If you believe that Options Greeks are limited to individual traders, think again. Sensitivity analysis of a portfolio of options by hedge funds and other money managers is also commonplace.

Let us now move on to the types of Greeks in options trading.

P.S. You can learn about the moneyness of options contracts by reading this blog: What is ATM/OTM/ITM in Options? It’ll be super useful ahead.

1. Delta

Delta Options Greek is simply the change in option price relative to the change in the price of the underlying asset. In other words, if the price of the underlying changes by Rs.1, the price of the option will change by Rs. 0.3 if the delta of the option Greek is 0.3.

Delta generally ranges from –1 to 1. Call options have a delta ranging from 0 to 1, while put options’ delta ranges from -1 to 0.

The closer the option is In-the-Money (Spot > Strike for call options & strike > spot for put options), the Delta will be closer to 1 (for call options) or -1 (for put options).

Delta is found by the following formula: ∂V/AS, where:

- ∂ = the first derivative

- S = the underlying asset’s price

- V = the option’s price

Delta in options trading is also known as the hedge ratio. If the trader knows Delta, then he/she can hedge their position by buying or shorting the underlying assets multiplied by Delta.

You could also say that Delta will help you determine whether an option will expire ITM, or the likelihood of it doing so.

2. Gamma

Gamma is the change in Delta relative to the change in underlying. As the underlying price changes, the options delta will also change in the gamma amount.

Long options, be it call or put have positive gamma. An option has the maximum gamma when it is at the money (strike price = spot price). However, gamma decreases when the option is deep in the money or out of the money.

3. Vega

Vega is an option greek that measures the change in the price of an option to the change in volatility of the underlying asset. If the volatility of the asset increases/decreases by a percent, the options price will commensurately increase/decrease by the Vega amount.

Vega Greek and option values are positively correlated. An increase in Vega will increase option value and vice versa. The trading fraternity considers the Vega Option Greek to be the most important and it generally helps option buyers as option premiums increase with the increase in volatility.

4. Theta

Theta is the change in the options’ price relative to the change in options’ time to maturity. Options are known as depreciating assets. As the time comes close to the expiry, option premiums lose their value.

Who does that? – It’s the Theta! If the option’s time to maturity decreases by any amount, the options price will change by the Theta amount. Theta is widely referred to as time decay.

Theta is negative for options. However, it may be positive only for some European options. Option sellers generally make optimal use of Theta by shorting the option at the start of the expiry, and towards the end, the option price might end up as nil, if it expires out of the money.

5. Rho

You could say that Rho is the least talked about and factored-in Options Greek. However, it may influence various options trading strategies if used correctly. Rho is the change in the options price relative to the changes in interest rates.

The interest rate here is generally the benchmark rate referred to as the risk-free rate. In practice, if the benchmark interest rates change by a percent, the option price will change by the Rho amount.

Why is Rho so significant? As the option prices are in general less sensitive to interest rates than changes in other parameters. Call options have a positive Rho, while put options have negative Rho.

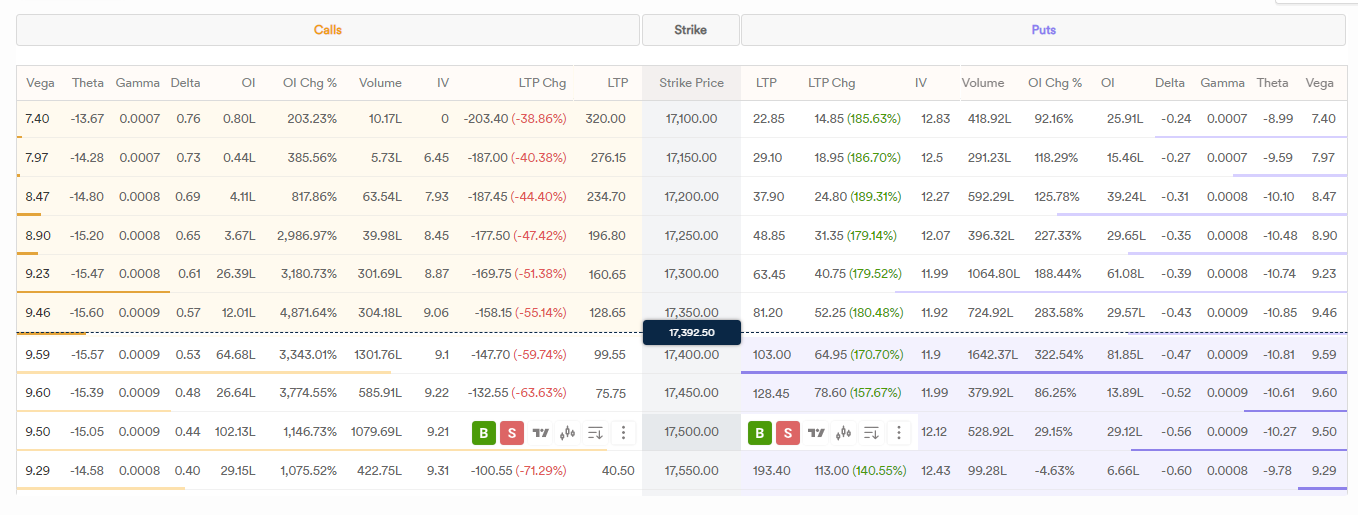

Where to Get Options Greeks for Trading?

Greeks are typically represented on an Option Chain. Think of the Option Chain as a place to view all available options contracts for a particular options stock. The image below will show you what Options Greeks look like on an Option Chain.

Showing Options Greeks on an Options Chain makes functional sense for traders because every crucial detail is visible in one place, meaning you can make informed decisions.

While conventional Options Chains don’t allow you to trade directly from them, Dhan’s Option Chain does. That’s why it is called Advanced Option Chain! Download Dhan to know more.

Conclusion

There it is: Option Greeks Explained! While there are other minor Greeks like Vomma, Zomma, Lambda, etc that also affect option pricing, the five Greeks mentioned above are the most significant. Option prices can be very volatile sometimes based on underlying assets and these Greeks change constantly and impact the options price.

As a trader, option pricing cannot be understood without understanding Options Greeks. We hope that these building blocks give a fairly good idea about how to approach options trading.

We at Dhan are constantly trying to make your options trading experience better with products like Options Trader Web with Custom Strategy Builder. Check out the video to know more.

FAQs

Q. What is Delta in Options?

Delta in options is the price of an options contract relative to the rise or fall in the underlying asset’s price.

Q. What is Gamma in Options?

Gamma in Options is the value you get by calculating the rate of change of Delta relative to the change in the underlying asset’s price.

Q. What is Vega in Options?

Vega in options is nothing but the change in the options contract’s price relative to the change in volatility.