The government has made provisions for individuals across tax brackets to save a part or whole of their taxes. That’s why efficient tax planning helps high-income earners in India maximize wealth and minimize tax liabilities.

While tax planning can be tricky, the right strategies can reduce your tax burden while staying within Indian tax laws.

You can optimize your taxes by using various provisions of the Indian Income Tax Act. Here’s a complete guide on effective tax optimization strategies for high-income earners.

Let’s dive in!

1. Section 80C Investments

A. Public Provident Fund (PPF)

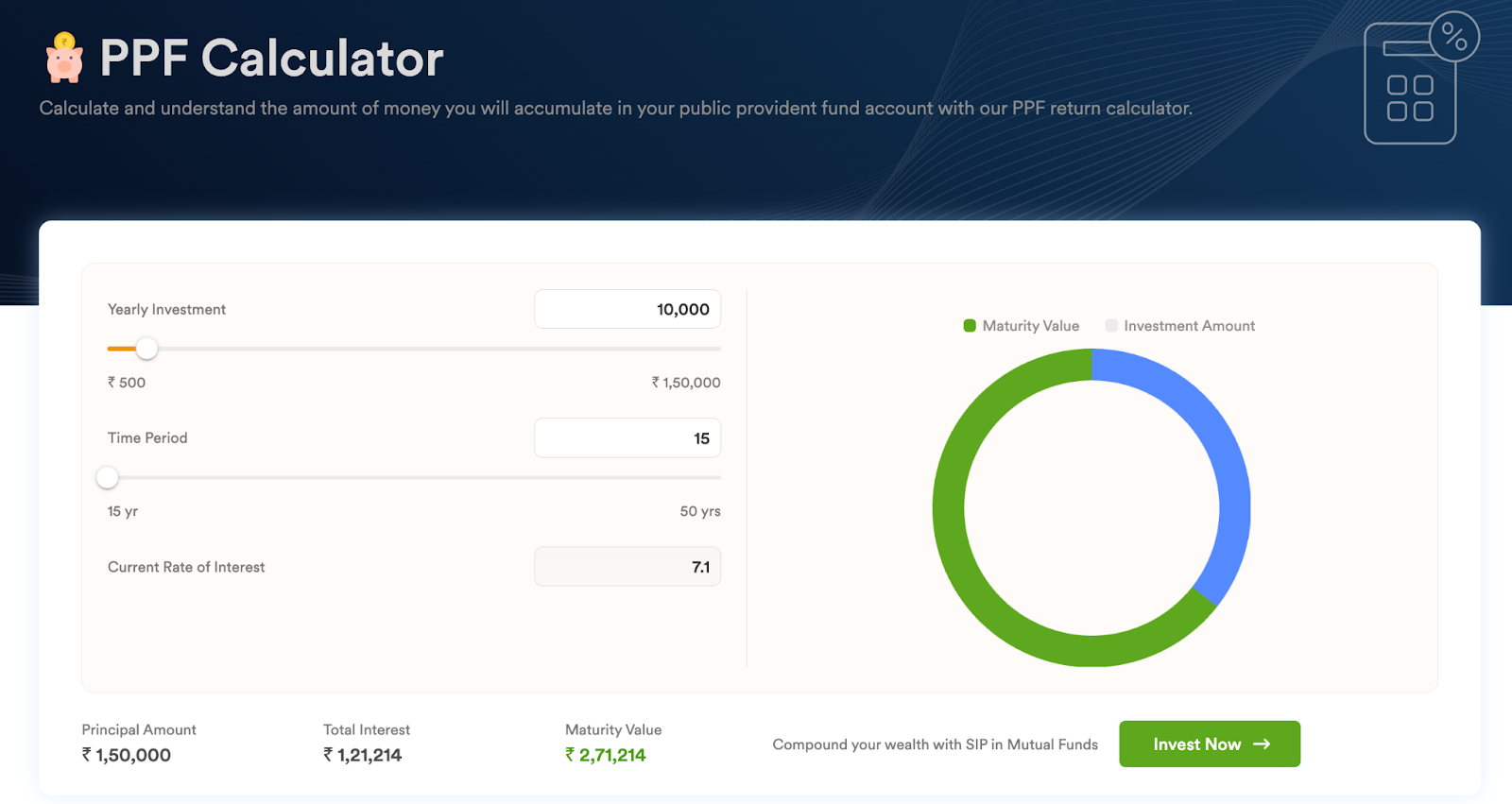

The PPF stands as one of the well-known tax-saving funds that carry fixed returns with government backing.

You have the option to invest up to ₹1.5 lakh, and you do not pay taxes on the interest you earn.

It requires a 15-year commitment making it a long-term investment, but it offers major tax advantages under Section 80C.

To get the most out of PPF investments by simply investing in it before the 5th of every month, specifically April.

Calculate your returns with this PPF Calculator

PPF interest is calculated as per the lowest balance in the account between the 5th and the last day of the month.

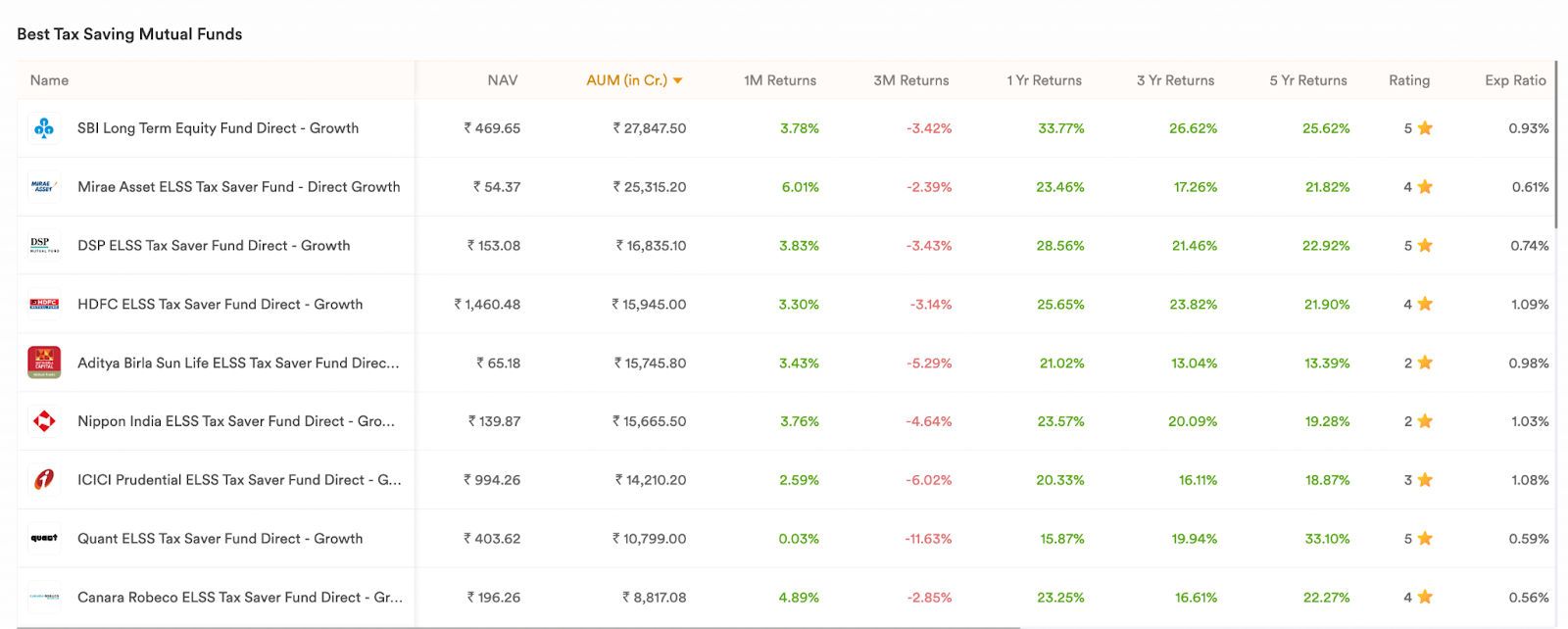

B. Equity Linked Savings Scheme (ELSS)

ELSS mutual funds list includes tax-saving equity mutual funds. They come with a compulsory lock-in period of three years.

According to Section 80C, investments of up to ₹1.5 lakh in ELSS funds qualify to get a tax deduction.

ELSS helps you save on taxes and gives you a chance for better returns because it grows with the market.

That’s why it’s more than just a tax-saving instrument – it’s a potentially solid investment for long-term goals such as buying a house or car.

C. Life Insurance Premiums

Tax deductions are also available for life insurance premiums under Section 80C. This includes policies for you, your spouse, and your children.

To get the most tax benefit, choose higher yearly premiums, up to the ₹1.5 lakh limit.

It’s important not to conflate life insurance or any other insurance with wealth creation.

2. Section 80D and Beyond

Health Insurance

Section 80D says that you can deduct health insurance premiums for yourself and your family.

You can get a claim of up to ₹25,000 for yourself. For your parents, you can claim another ₹25,000 if they are below 60, or ₹50,000 if they are over 60.

National Pension Scheme (NPS)

The NPS offers an additional deduction of ₹50,000 under Section 80CCD (1B). This comes over and above the ₹1.5 lakh limit falling under Section 80C.

The government backs the NPS scheme as it aims to provide retirement income, and it’s a great tool for long-term savings and tax optimization.

3. Capital Gains Tax Planning

Section 54 and 54EC

You can cut your capital gains tax when you sell a residential property by putting the money into another home under Section 54.

Another option is to invest in specific bonds like NHAI or REC within six months of selling to claim an exemption under Section 54EC.

Indexation Benefit

High-income earners can use the indexation benefit to adjust the cost of acquisition of assets for inflation, thereby lowering capital gains.

The Cost Inflation Index (CII) provided by the government helps in updating the asset’s cost to its current value, cutting down the tax liability.

4. Other Ways to Optimise Tax

Utilising Hindu Undivided Family (HUF)

Families can create a HUF for themselves in order to pool assets and income. This will cut individual tax bills.

A HUF is treated as a separate entity for tax purposes and enjoys the same tax perks as an individual. This makes it a strong tool for high-income earners.

Donations and Charitable Contributions

Donations to approved charitable institutions are tax-deductible under Section 80G. Contributions to specific funds like the Prime Minister’s National Relief Fund qualify for a 100% deduction, while others may be eligible for 50%.

Real Estate and Housing Loans

Interest paid on home loans for self-occupied properties is deductible up to ₹2 lakh per year under Section 24(b).

Moreover, the repayment of the principal amount qualifies for a deduction as per Section 80C.

These deductions make home loans a good choice to save taxes while investing in real estate.

Special Considerations for High Net Worth Individuals (HNIs)

Here are special considerations for HNIs in India.

Double Taxation Avoidance Agreement (DTAA)

For HNIs with income from foreign sources, the DTAA prevents double taxation on the same income.

This agreement between India and other countries ensures that HNIs are not taxed twice on their foreign income, providing clarity on tax residency and allocation of taxing rights.

Foreign Assets Reporting

HNIs should tell about their foreign assets and income to Indian tax authorities. Compliance includes filing forms like the Foreign Assets and Liabilities Information (FAL), Tax Residency Certificate (TRC), and Foreign Tax Credit (FTC) details.

Proper documentation, such as bank statements and contracts, is crucial for supporting their foreign income and tax position.

Conclusion

Smart tax planning is crucial if you have a high income. You can reduce your tax bill by benefiting from different sections of the Income Tax Act, putting money in tax-saving funds, and making informed investment decisions.

Get started, make smart choices, and grow your wealth through smart tax optimization.

Understanding these strategies will not only help you save on taxes but also guide you in making better financial decisions that will help you build wealth over time.