One of the first things most of our parents or guardians must have said is to open an FD as soon as we start earning—to invest.

Fixed Deposits (FDs) have been one of the most straightforward investment options, especially for those looking to safeguard their savings while earning stable returns.

But what exactly is a Fixed Deposit? Let’s find out.

What is a Fixed Deposit?

A Fixed Deposit is a financial instrument offered by banks and financial institutions where you deposit a lump sum of money for a fixed period at a predetermined interest rate. At the end of the term, you receive your initial investment plus the accrued interest.

Unlike a savings account, FDs lock in your funds for a specific duration, which can range from a few months to several years.

How Do Fixed Deposits Work?

The concept of how an FD works is pretty simple. When you open an FD account in a bank, you agree to deposit a certain amount for a set period at an interest rate specified by the bank.

During the term, your money earns interest, typically compounded quarterly or annually. Once the tenure ends (known as maturity), you can withdraw the full amount, including the accumulated interest.

Types of Fixed Deposits

Fixed Deposits come in different forms to suit various needs:

- Standard Fixed Deposit: The most common type, where the principal amount is locked for a chosen period, and interest is paid upon maturity.

- Tax-Saving FD: A special type of FD with a 5-year lock-in period that offers tax benefits under Section 80C of the Income Tax Act.

- Cumulative and Non-Cumulative FDs: In cumulative FDs, interest is compounded and paid at the end of the term, whereas non-cumulative FDs pay out interest periodically (monthly, quarterly, etc.).

- Senior Citizen FD: Offers higher interest rates specifically for individuals above a certain age (usually 60 years and above).

It is important that you’re aware of each kind of Fixed Deposit to choose the right one according to your financial goals.

Interest Rates on Fixed Deposits

Interest rates on FDs vary based on the financial institution and tenure chosen. They typically range between 3% to 7%, with senior citizens often receiving an additional 0.25% to 0.5% on their deposits. Comparing rates across banks can help maximize your earnings.

Here’s a table of the most popular FDs and their interest rates for 2024.

| Financial Institution | Avg. Interest Rate (per annum) |

| HDFC Bank | 6.60% |

| ICICI Bank | 6.70% |

| Kotak Mahindra Bank | 7.10% |

| Bandhan Bank | 7.25% |

| Axis Bank | 6.70% |

| Bank of Baroda | 6.30% |

| SBI | 6.80% |

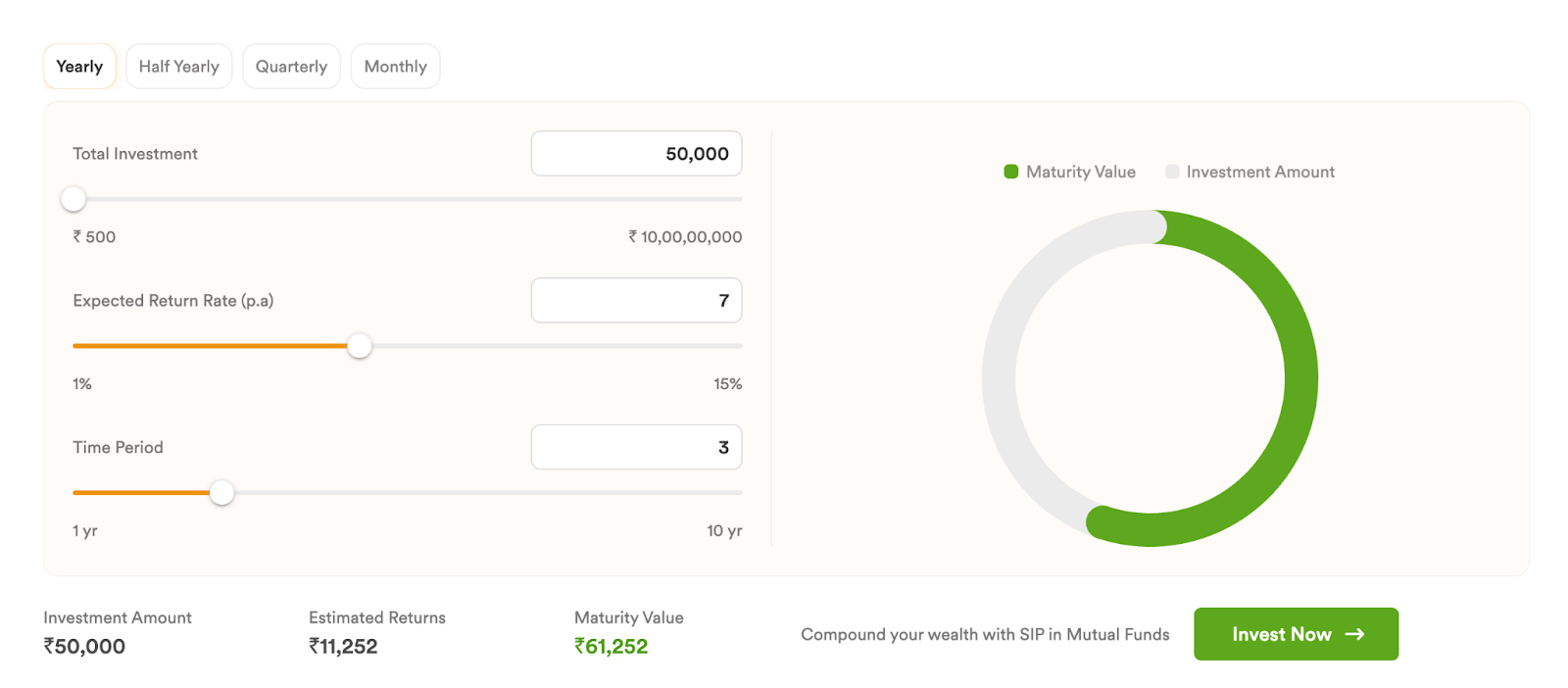

FD Calculator

Find out the investment returns & expected return rate with this FD calculator:

Pros and Cons of Fixed Deposits

With evolving financial markets and diverse investment options, it’s essential to weigh their advantages against other strategies to ensure they align with your financial goals.

Pros:

- Safe and Secure: Low-risk with guaranteed returns.

- Flexible Tenures: Choose a period that suits your needs.

- Predictable Earnings: Fixed interest rates provide stability.

Cons:

- Lower Returns: Compared to equity or mutual fund investments.

- Penalties for Premature Withdrawals: Fees may apply if you break the deposit early.

- Inflation Impact: Returns may not always keep up with inflation, impacting real earnings.

Is Fixed Deposits the Right Choice for You?

With assured interest rates and capital protection, FDs are ideal for those seeking stable growth without market volatility. However, they may not suit everyone.

The returns often lag behind inflation, limiting long-term purchasing power. For investors looking to build wealth or beat inflation, diversified options like mutual funds or stocks could be more beneficial.

So, it is crucial to consider your risk tolerance, financial goals, and time horizon before deciding if FDs align with your strategy:

Investment options like Mutual Funds generally offer more advantages than fixed deposits (FDs) in terms of returns, flexibility, and diversification.

Mutual Funds also offer better liquidity, as they can be redeemed at market value without penalties, unlike FDs which often charge fees for early withdrawals. Mutual Funds are tax-efficient, as long-term capital gains may be taxed at lower rates compared to the interest on FDs, which is taxed at the investor’s income tax rate.

Conclusion

Fixed Deposits offer a straightforward way to grow your savings with minimal risk. Whether you’re just starting out or looking to diversify your investment portfolio, FDs provide a safe and predictable option for achieving your financial goals. Make sure to compare different institutions and FD types to find the best fit for your needs.

Over the past decade, new investment options have emerged, offering higher returns and innovative alternatives to traditional choices like fixed deposits. Mutual Funds have historically given better returns, and are now easily accessible and manageable.

Invest in Mutual Funds at 0% Commissions and earn 1% higher returns on your investment. To start, open a Free Demat A/c today!

FAQs

- Can you break an FD before its completed tenure?

While FDs are meant for long-term saving, emergencies can happen. Most banks allow premature withdrawals but may charge a penalty or reduce the interest rate. It’s essential to check the terms before breaking an FD early.

- How to Open a Fixed Deposit Account?

Opening an FD is a straightforward process. Every bank might have slightly different procedures but overall the following steps are required:

- Visit a Bank: Either physically or through online banking.

- Choose the Tenure and Amount: Based on your financial goals.

- Submit KYC Documents: Identification and address proof are needed for verification.