Debt often carries a negative connotation with it. People generally tend to believe that debt is something you incur. However, there’s the concept of good debt and bad debt. Debt mutual funds fall in the category of good debt. Let’s dive into what is debt mutual fund!

What Is Debt Mutual Fund?

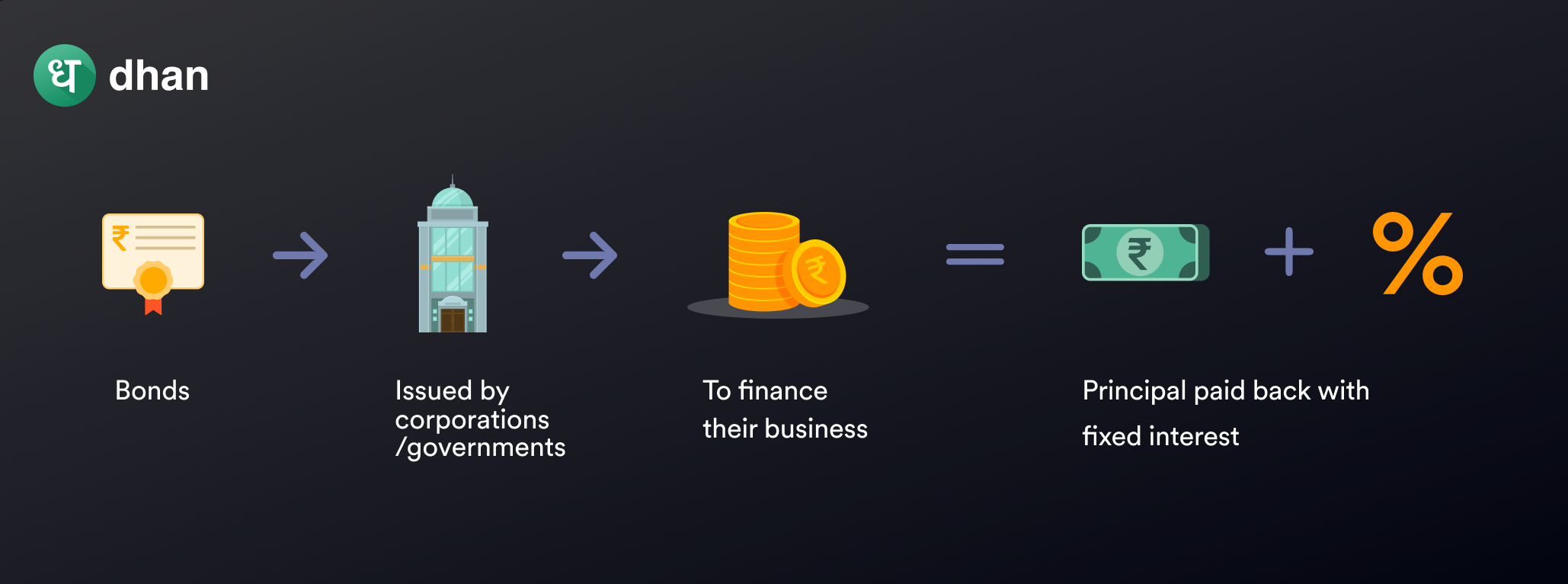

A debt mutual fund is a type of mutual fund scheme that invests in bonds, commercial paper, certificates of deposit, treasury bills, and other securities that generate a fixed income.

These fixed-income securities are generally issued against a loan by corporations and the government that want capital to meet their business needs.

If there’s a loan involved, there must be interest in the mix as well. That’s why the ones who issue the bond attach a fixed interest rate on top of the borrowed capital.

Given all of this information, you could look at debt funds in two ways. Because the interest income is fixed, there’s significantly lower risk involved in debt funds than, say, investing in equity funds that hold volatile shares in their portfolio.

This safety, albeit attractive, comes at a cost (literally). The returns that a debt fund generates typically range from 6-8% over the short to medium term. We’ll talk about the consequences of these returns later on.

Either way, debt funds are preferred by investors who tend to follow a low-risk investment strategy. In fact, many risk-averse investors like to compare traditional fixed deposits with debt funds.

In most cases, debt funds are known to generate better returns than FDs, although they may not be as safe as their traditional counterparts.

Now that you’re aware of what is debt mutual funds meaning, let’s move on to understanding how a debt fund operates.

How Does Debt Mutual Fund Work?

First things first – a debt fund is offered to investors by several Asset Management Companies (AMCs). As the name suggests, AMCs manage people’s money with the aim of generating returns.

They do so by allocating the money in and across a variety of financial instruments based on an objective. In the case of debt funds, the financial instruments include:

- Bonds

- Commercial paper

- Certificates of deposit

- Treasury bills

The investment objective may be to generate consistent returns with low risk by investing in the debt instruments mentioned above. But not every debt fund invests in every debt instrument.

The instruments are chosen to cater to the investment objective of the fund, which oftentimes rests in generating consistent returns by investing in one particular theme of debt instrument.

For example, a money market fund would invest in money market securities that mature overnight to 12 months. A corporate bond fund would primarily invest in corporate bonds that mature in months to years.

The decision to buy and sell these debt securities rests upon a fund manager who’s an expert in the financial markets. The fund manager doesn’t act alone – they generally have a team of analysts helping them.

Professional management is one of the most attractive elements of a debt fund or any mutual fund, for that matter. You won’t have to do the legwork – a team of experts will do it for you.

That said, the management team charges a fee in the form of an expense ratio. For debt funds, this is typically low compared to other mutual funds like equity funds.

Types of Debt Mutual Funds

| Type of Debt Fund | What it invests in | Average returns |

| Banking & PSU fund | Bonds issued by banks & PSUs with varying maturity | 5-6% |

| Corporate bond fund | Bonds issued by corporates with varying maturity | 6-7% |

| Credit risk fund | Bonds having a low credit rating with varying maturity | 5-6% |

| Dynamic bond fund | Bonds with varying maturity and interest rates | 6-7% |

| Gilt fund | Bonds issued by the government with varying maturity | 6-7% |

| Liquid fund | Bonds that mature in up to 91 days | 3-4% |

| Low duration fund | Bonds that mature in up to 12 months | 3-4% |

| Overnight fund | Bonds that mature overnight | 3-4% |

| Short duration fund | Bonds that mature in up to 3 years | 4-6% |

| Ultra-short duration fund | Bonds that mature in 3-6 months | 3-4% |

1. Banking & PSU Fund

Banks and companies that fall under Public Sector Undertaking (PSU) issue bonds to finance their business. Think of companies like BPCL, ONGC, SBI, and others.

These bonds are generally highly rated and as a result, the debt fund that invests in them is viewed as superior to others. At the same time, banking & PSU funds can generate relatively solid returns.

2. Corporate Bond Fund

Companies like Reliance, TCS, Wipro, & others often issue bonds for the short to medium term. These bonds typically carry a good rating but are viewed as riskier than banking & PSU bonds because of the private companies in question.

Furthermore, corporate bonds are known to carry lucrative interest rates. This means that the debt funds that invest in them may also have the potential to generate solid returns.

3. Credit Risk Fund

Some bonds have a high credit rating. Others don’t. Credit risk mutual funds invest in bonds with a subpar credit rating. This puts the investment at a higher risk than other debt funds. But it has the potential to generate decent returns if everything works out.

4. Dynamic Bond Fund

Certain debt funds have the freedom to invest in bonds with varying maturity and interest rates. Dynamic bond funds are one of them. They can hold and change their portfolio based on economic conditions and changing interest rates.

5. Gilt Funds

The government has a high credit rating. The government also issues bonds. These are the bonds that gilt funds invest in exclusively.

Considering the high credit rating that government bonds possess, gilt funds that invest in them are known to be relatively less risky than others.

6. Liquid Fund

There are bonds and other money market securities that mature in 91 days or less. That’s what liquid funds invest in. The logic is that debt securities that mature sooner carry lower risk.

Furthermore, such securities are far more liquid than others. This is why liquid funds are used in continency funds, emergency funds, and other buckets in an investor’s portfolio.

7. Low Duration Fund

A low-duration fund is a basket term used to describe any debt fund that invests in securities that mature in 12 months or less. Such funds typically have a low-risk profile and mirror the risk with predictable returns.

8. Overnight Fund

This may be one of the most unique debt funds on this list because overnight funds invest in bonds that mature overnight, that is, in 24 hours or less.

This means that they carry low risk and generate significantly low returns, which is most commonly used as a pitstop in a Systematic Transfer Plan (STP) or to beat a bank savings account.

9. Short Duration Fund

This is another basket term used to describe debt funds that invest in securities that mature in 3 years or less. While these debt funds fall in the relatively risky category, the returns they can generate are predictable.

10. Ultra-Short Duration Fund

There are bonds that mature in 3 to 6 months. This is what ultra-short-duration funds invest in.

Advantages & Disadvantages of Debt Funds

| Advantages of debt funds | Disadvantages of debt funds |

| Relative low low risk | Relatively low returns |

| Suitable for short to medium-term goals | Unsuitable for long-term wealth creation |

| Potentially better returns than FDs | Higher risk profile than FDs |

| Lower expense ratio than equity funds | Returns not as high as equity funds |

Who Should Invest in Debt Funds?

By now, you must’ve understood what is debt mutual fund – debt funds invest in fixed-income securities that are generally low-risk instruments. That’s why the returns they generate are also typically low.

These factors make debt funds suitable for investors who prefer a stable, predictable asset for wealth creation. That’s why debt funds’ are known to be useful for short-term wealth creation goals.

There’s also a school of thought that pits FDs against debt funds by comparing the returns. In principle, this can be true but you must also keep in mind that debt funds are market-linked assets.

They carry a degree of risk, albeit relatively lower than other mutual funds, that must still be taken into account before planning a portfolio or doing asset allocation.