Did you hear the whispers about a central bank digital currency (CBDC)/ Digital rupee and how the RBI is planning to work on it? In today's blog, let's discuss the digital rupee and why RBI strides to make it work.

Introduction

Going digital is no longer a trend – it’s a necessity. Right from grocery shopping to sending money to your family, everything can be done online. The key enabler of digital money is technology, especially in India where UPI is used by everyone for everything.

Keeping with the theme, the RBI has another spanner in the works in the form of the Digital Rupee. But how is it different from UPI or even cryptocurrencies? Let’s see.

What is CBDC Digital Rupee?

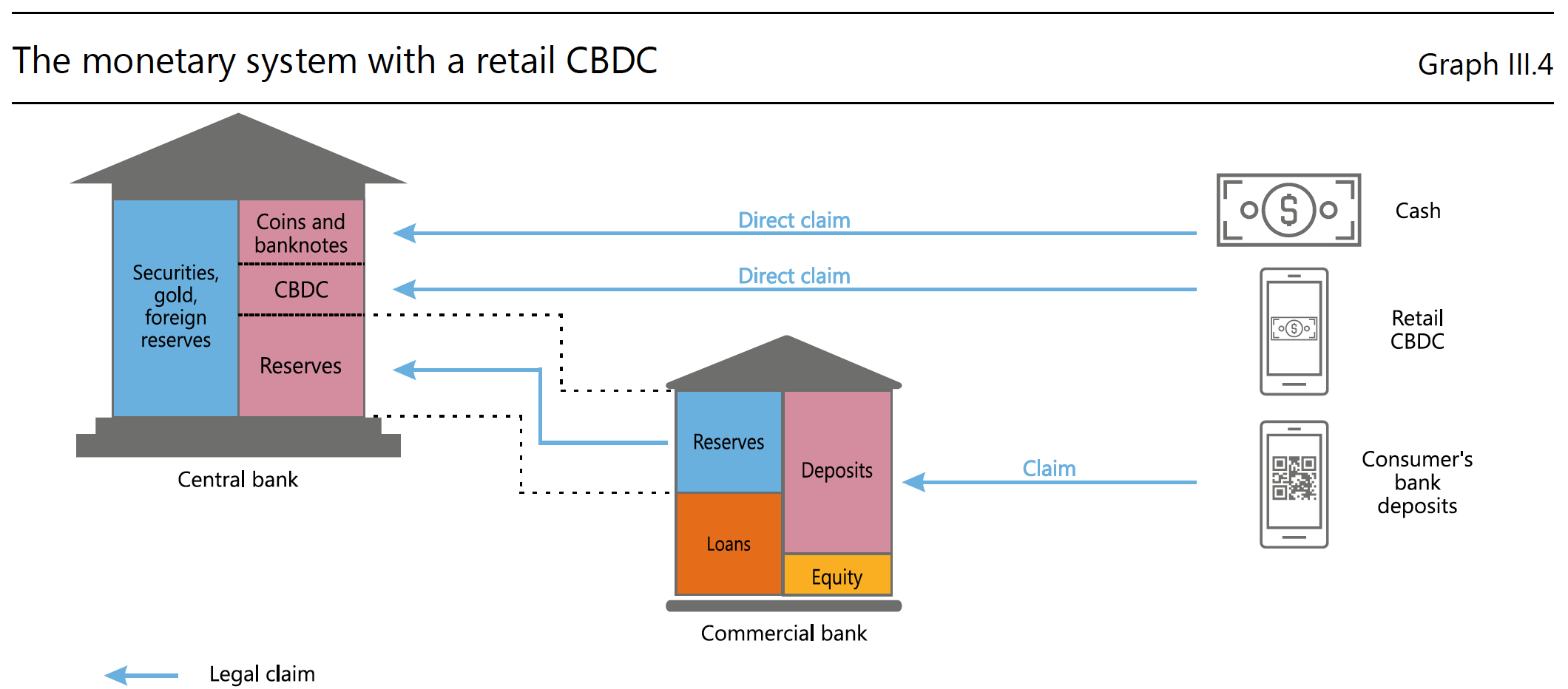

As interesting as it might sound, a Central bank digital rupee (CBDC) is just like UPI but much simpler, more sophisticated, and techy. How? When you transfer money to someone via UPI you have to send it through the bank and it’s a bank transaction.

You > Bank > Receiver's bank > Them

But in the case of e₹, you don’t need banks at all. In fact, you can directly transfer money to another account. Or as the papers say

“Imagine a UPI system where CBDC (Central Bank Digital Currency) is transacted instead of bank balances, as if cash is handed over — the need for interbank settlement disappears.”

If you too are wondering how much an e₹ costs, the govt. is planning to introduce it 1:1 i.e one rupee will be equal to one e₹.

If it’s not like UPI and works directly, how does it differ from cryptocurrency, and are they the same?

Difference Between Digital Currency and Cryptocurrency?

If you have ever noticed our currency note, it states/ promises that – RBI will pay whoever is the bearer of the note, a sum of ₹xx. It is legal tender i.e. can be used to pay for any transaction in India.

Each currency note is essentially a claim on the RBI. Central Bank Digital Currency (CBDC) states the same but in a digital form.

Similarly, RBI ensures that the CBDC digital rupee ( e₹) stores a similar value and is backed by RBI as well.

In simple terms, it’s a rupee note but in a digital form. Sounds simple and are thinking why would RBI launch CBDC as much of the complexity has already been taken care of by UPI?

Why RBI is Thinking to Launch the Digital Rupee?

CBDC digital rupee has multiple use cases and there are multiple reasons why CBDC can be helpful for the Indian economy.

1. Programmable Payments (DBT)

“Programmable money” is, without a doubt, one of the biggest buzzwords in blockchain world. Despite the fact that everyone seems to talk about it, we lack a clear definition and hence a common understanding of it.

The term Programmable Payments means payments that are automatically executed once certain conditions are met. Thus, these payments are automated and follow predetermined logic. Programmable payments already exist in today’s banking system, for example, in the form of standing orders and direct debits.

But now this can be used in different daily life scenarios like subsidies for sectors like agriculture, where subsidies for fertilisers could be transferred via the CBDC route. This CBDC could only be accepted at authorised fertiliser outlets, ensuring there is minimal leakage in the subsidy program.

Moreover, programmable payments can also be used in industrial supply chain ecosystems, by organisations for employees’ expenditure and more.

2. Cross-Border Transactions

CBDCs could be used for faster (or the fastest) cross-border remittance payments. With major major economies of the world, India could create the necessary infrastructure and arrangements for CBDC transfer and conversion.

Let us understand with a recent example- The sanctions imposed on Russia after the invasion of Ukraine were multiple – Russian participants were removed from SWIFT, the dollar payment network, etc. The purchase of Russian debt was also restricted which cuts Russia off from the financial markets.

Over $600 billion in gold, dollars, and other currencies had been accumulated by Russia. Under these sanctions, the USA, UK, and EU frozen half of these reserves. A significant chunk of our own reserves ($ and gold) are held overseas.

Such cases create an uncomfortable situation where if India does something that the West doesn’t like, the financial system may collapse.

In this case, CBDC remittances could happen in real-time, rapidly reducing the time required for the payment to be received by the intended receiver.

Apart from transacting with the economies, CBDC can also be used for retail payments:. A CBDC could also offer offline payments as part of its universal access attributes.

Retail CBDC distributed by the RBI and commercial banks would have to be held in electronic wallets/ accounts by the end users. This would enable payment means between the following:

• B2B: Here businesses can exchange CBDC between their corporate account digital wallets

•C2C: Consumers can exchange CBDC between their digital wallets

• C2B: Consumers can use CBDC to pay for products and services

Does this concept sound similar to cryptocurrencies? Or should I say Cry-ptocurrency. If yes, what’s the difference and why not just use cryptocurrency.

Is CBDC Digital Rupee Just Like Cryptocurrency?

Cryptocurrency does not come with any underlying claim to any asset. Its value is based entirely on public perception (speculation). Unlike cryptocurrencies where Elon Musk can take your coin to the moon and back to earth, the value of CBDC remains stable.

Other cons that crypto has are illegal transactions, and multiple instances of fraud, but a currency with the backing of a central bank like RBI is much safer. e₹ can also be exchanged for ₹.

And other pros like DBT which we talked about earlier and cross safe cross border transactions

Did you know that: About 90% of world's central bank are pursuing Central bank Digital Currency (CBDC) Project.

Few exciting questions might pop up in your head 🧠

- If it sounds so safe will RBI give interest on CBDC?

When you park your funds in the bank gives you interest as it uses your money for giving out loans, etc. But here CBDC solves a purpose: if these pay interest, many people would shift their funds to CBDC and banks would struggle to raise deposits.

This will affect the lending and deposit rate and also affect banks’ margins which eventually brings instability to the financial system

That’s a wrap for this from us today. What did you think of this edition of the CBDC digital rupee? Is there something we can cover for you? Let us know on Twitter.

We’ll see you in the next one!

Wait, loved what you just read? Do you want to read more such interesting stories. Have a look at these ones

- Everything you need to know about UPI!

- The Complete Guide to Bollinger Bands Indicator

- Business Analysis of Borosil Renewables

Or if reading about curriences just made you more interested you can read everything about Forex curriences here.