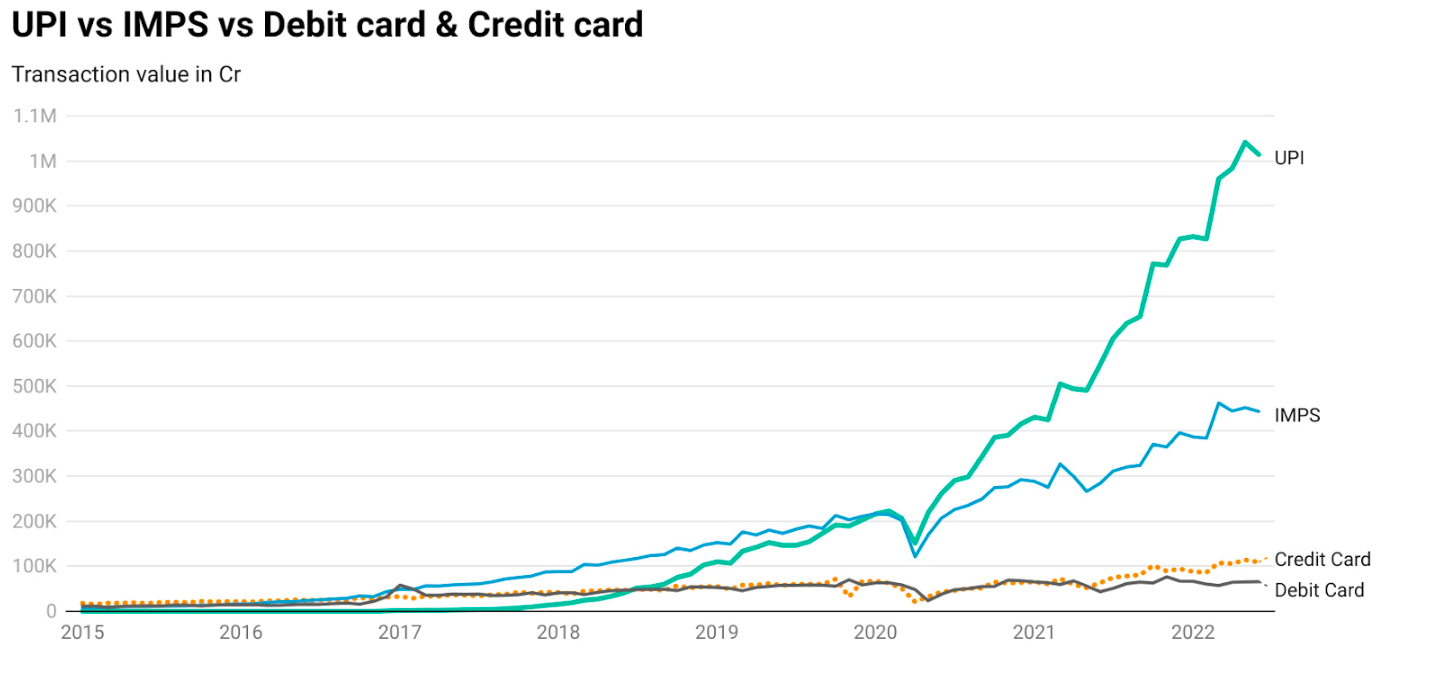

India is living in the future in terms of the instant payment system, we left the US, the UK, and Australia far behind. Thanks to UPI and its lightning-fast transfer speed. It feels like it was with us since inception!

Did you know, when you send Rs. 1000 to someone, Rs. 2.5 has to be incurred by the platforms to provide you with a seamless ecosystem. So, there are no free lunches. The question now is – who’s earning in this ecosystem and why is the government ready to spend from its pocket?

What is Happening with UPIs in India?

UPI has been one of the greatest revolutionary technologies that we have invented and since then, its usage of it has skyrocketed.

After the recent policy by RBI to modify UPI, IMPS & NEFT charges, there was a fuss around “Should UPI be free or not” and what innovations we can expect? So before we start diving deep into UPI’s, let’s see how and why UPI was invented.

The Birth, the Rise, and the Shine of UPI

UPI was first launched in 2016. It was piloted by the National Payments Corporation of India (NPCI) and it was launched along with 21 member banks by Raghuram G. Rajan, then RBI governor.

UPI’s target audience was basically everybody that uses digital methods of transferring money. Be it net banking or IMPS. UPI is a critical factor in the country’s evolving cashless ecosystem.

What is UPI and How Does it Work?

The full form of UPI – Unified Payment Interface. It is a smartphone application for transferring money between bank accounts. The platform allows users to link their bank accounts held by different banks into a single UPI application and transact between them using their mobile phone numbers. i.e transferring funds just by your phone numbers or UPI ids.

The UPI Platform is a system that operates from multiple bank accounts in a single mobile application from participating banks, combining multiple banking features such as merchant payments and fund transfers all under one roof.

The National Payments Corporation of India (NPCI) developed a single-window mobile payment system. Every time a customer initiates a transaction, they do not have to enter their bank details and other sensitive information. New features have been added to UPI, such as In-App payments and QR code payments.

We all are used to payment apps like Google Pay, Paytm, Phonepe, and now CRED Pay. These apps have become a crucial part of our lives. The transaction on these apps takes place by UPI, a single-interface payment system developed by the National Payment Corporation of India (NPCI).

Every UPI transaction includes 5 parties. The following image represents how the UPI framework works when you buy something from let’s say amazon and select payment mode as google pay.

Till now we have witnessed how UPI (Google Pay, Paytm & PhonePe) have added value to our lives and now you also know that the government is ready to spend on this infrastructure. So now let’s understand why there was a need for UPI.

Why was UPI Born and Why is it Rising?

The need for UPI was simplicity – to provide a simple solution for all those complex transfers.

Netbanking and card payment was with us for a pretty long time. It was just the complexity i.e to enter the IFSC code, bank name, and other 100 questions that needed to be filled. This made us stay away from online transfers for a very long time.

To be precise in 2011, on average there were only 6 transactions per person in an entire year! And now your Google pay history says it all.

Digital Economy

UPI usage has spread more than the covid in the last 2 years! Reason? One of the reasons is that the RBI has asked to remove Merchant Discount Rate (MDR) on UPIs which made the platforms like Amazon, Ajio, and Flipkart use it more. Because handling cash is too difficult.

Did you know: Handling of cash by govt takes 2% of our GDP (2.7 lakh crore)

Unregulated Cash

UPIs are linked to bank accounts, and payments done via banks are regulated. This means that black money which is floating outside can be controlled as a maximum number of people would use online transfers and acceptance of cash will be reduced.

How UPI Can Contribute to the Growth of Economy

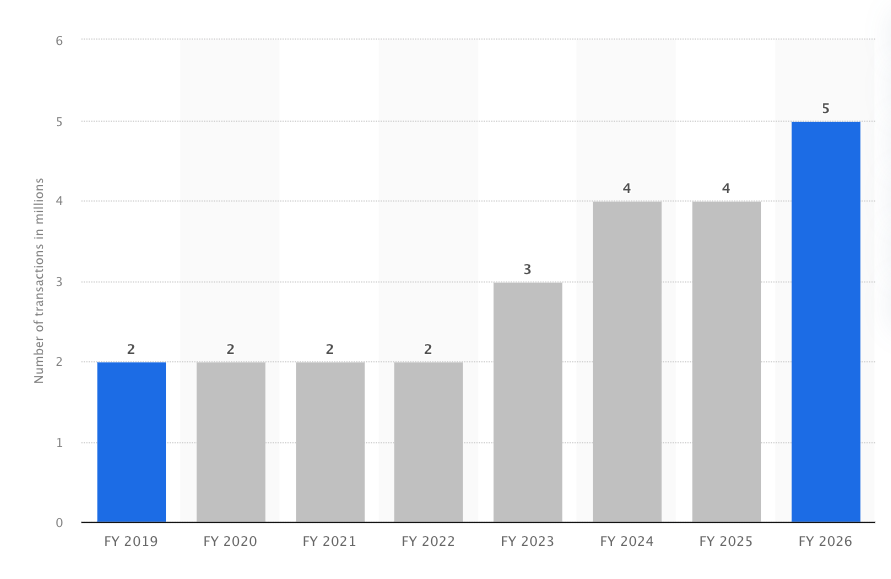

In 2021, instant payments saved India $12.6 billion in payment costs. According to a Cebr economic research study, these cost savings enabled India to unlock $16.4 billion in economic output or 0.56 percent of its GDP.

By 2026, India’s instant payment solutions is expected to generate an additional $45.6 billion in economic output, equivalent to about 1.12 percent of India’s GDP.

Till now it is pretty evident that UPI has made a massive impact on the Indian payment system. As we discussed earlier that for every transaction of Rs. 1000. Rs.2.5 is spent to manage and maintain this infrastructure.

Furthermore, as the new RBI circular suggests modifying UPI, IMPS & NEFT charges, let’s see why UPI does not sound free or why should it be free?

Should UPI Be Free and Growth Opportunities for UPI?

Banks aren’t happy with UPI being free

UPI’s cost is next to nothing. Why because banks are paid in two ways: first, the government subsidizes them with 1,300 crores a year, enough to meet costs and more. But banks get much larger amounts by just keeping a larger amount of float money in the banking system.

A UPI system costs 400 crores to the company that manages the transaction flow and settlement (NPCI) a year at the very max.

The amounts earned in the float are close to 100,000 cr and then, banks get around Rs. 1,500 cr. from the government for running the UPI infrastructure.

Paralyzed Innovation- due to high CAC

Google Pay and PhonePe account for nearly 80 percent of the digital payments market in India. However, these platforms are indifferent, nor do they have anything that makes them appealing to users.

Payment companies are spending a lot of money on marketing and educating users, and vendors. For example, Google Pay spent millions in cash back to onboard customers.

These spends are known as customer acquisition costs (CAC). Payment markets are operated mainly by a few big players and any bigger players can’t afford to blink; if they slack, the competitor will eat into their market share.

Due to high CAC, it’s difficult for a new player to enter this market and build its audience. If you’re wondering why CRED recently launched CRED Pay then don’t forget CRED is a part of the fintech world for a long time with a billion-dollar valuation.

Why Payments Should be Free – Banks have Big Bellies

The amount of money in savings accounts pays around 3.5% to 4% a year or current accounts which pay no interest are the float for a bank. As of right now, even overnight parking in RBI earns much more than this money:

If banks simply park their funds with RBI they can earn 5.15%, but banks have way better avenues to lend and earn even more on it.

Here’s how much money banks make on the float (current plus savings accounts) right now. Compare this to what NPCI spends on all UPI+everything else.

Float generates nearly 140,000 crore rupees of income for banks. This float income is only available to banks and NBFCs don’t have such accounts or float income. Given this, the float income is primarily used to pay for payment infrastructure.

Near-time innovations expected in Payments/ UPI

We Indians are loving UPI because if its – Low transaction cost, Speed, and low failure rate. It has been a part of us for a long time. Inspired by us, many other countries are planning to launch the same in their payment infrastructure.

But as UPI and technology are timeless pieces of innovation, what should we expect in the upcoming times?

UPI x Credit Card!

What if credit cards could be used to make UPI payments? That’s right. Using an old and boring payment instrument to pay for a new, and cool payment protocol.

Soon you can link your credit card, probably RuPay’s Credit card to pay your bills.

Rise in the Volume of Credit Card Transactions in India

According to studies, customers tend to spend more when he/she is using a credit card. Linking credit cards to UPI will provide a seamless experience to users and I think probably that’s the reason why CRED introduced CRED Pay! (Just thinking out loud)

UPI 123

No internet on mobile is required for a transaction. You will be able to make a transaction through a missed call.

UPI Lite

A Wallet like PayTM where you can store up to Rs 2000 for smaller transactions up to Rs. 200 per time (without any internet connectivity)

This brings more to the users who do not have internet access and adds more to UPI’s system. It doesn’t end here. A few months back the government of India also started a new campaign called JAM trinity to increase boost the economy, and digital space.

Global Usage of UPI

The UK and recently France and Singapore have also talked about adopting the UPI system.

In the future, it is quite likely: That we will be able to travel without the hassle of exchanging currencies with the help of this system.

Conclusion

As mentioned earlier, there are no free lunches as the government is paying to keep this payment ecosystem running and banks are earning enough with floats and 1500 cr which are allocated to them.

This indicated it’s better that UPI should be free because the idea is to promote more and more people into digital payments, which allows for far greater things to happen on top of this infrastructure and payment apps earn with on every transaction (like electricity, water or such) Because more the transaction better the economy!

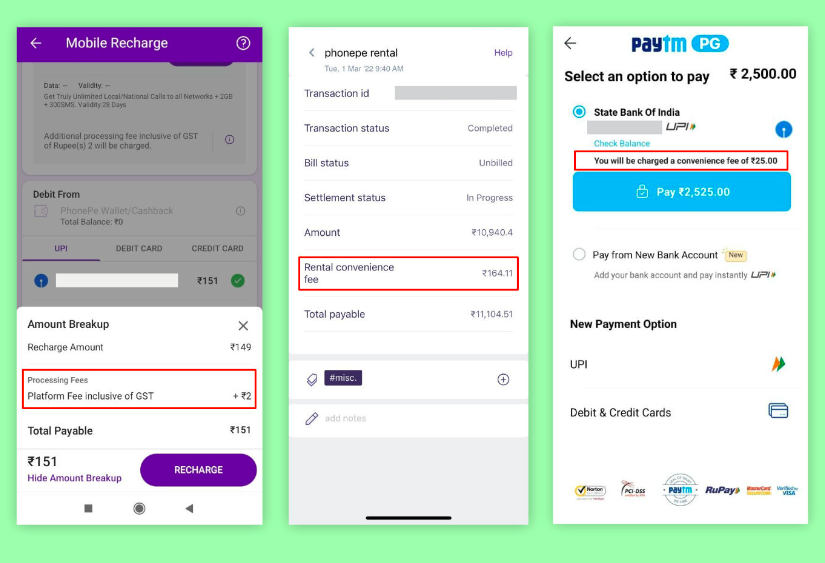

Keeping UPI free will add more value to the ecosystem and there should be more fintech platforms entering this segment to reduce the monopoly of big fish. Because there are only a few big players they might start charging convenience fees to their users. For example:

Payments through UPI are both safe and fast, and they have made our lives easier and more convenient.

UPI will facilitate transactions across countries while providing a powerful risk management system in case of fraud. The UPI transactions are growing at a dynamic rate and have great growth potential. And can contribute significantly to India’s GDP.

India will be a far better place for payments if UPI is kept free. Payments with UPI are already the cheapest and fastest so it’s important to keep it free so, more new fintech players can enter the payment markets and the scope of innovation stays in the hands of transactions.

Let us know if you have any thoughts or feedback about what we should cover next.

See you in the next one 🙂

You can read more such interesting stories like:

- Business analysis of – Amber Enterprises

- Business analysis of – Borosil Renewables

- Expert Opinions on Investing, Commodities, and trading psychologies.

Disclaimer: This blog is not to be construed as investment advice. Trading and investing in the securities market carries risk. Please do your own due diligence or consult a trained financial professional before investing.